The real estate policy reforms announced in March will impact the residential housing triangle of property investors, first home buyers, and renters. Let’s look at the bright-line test, supply, and tax deduction reforms set in motion, and how they’ll affect Christchurch property investors.

Bright-line test extended to ten years

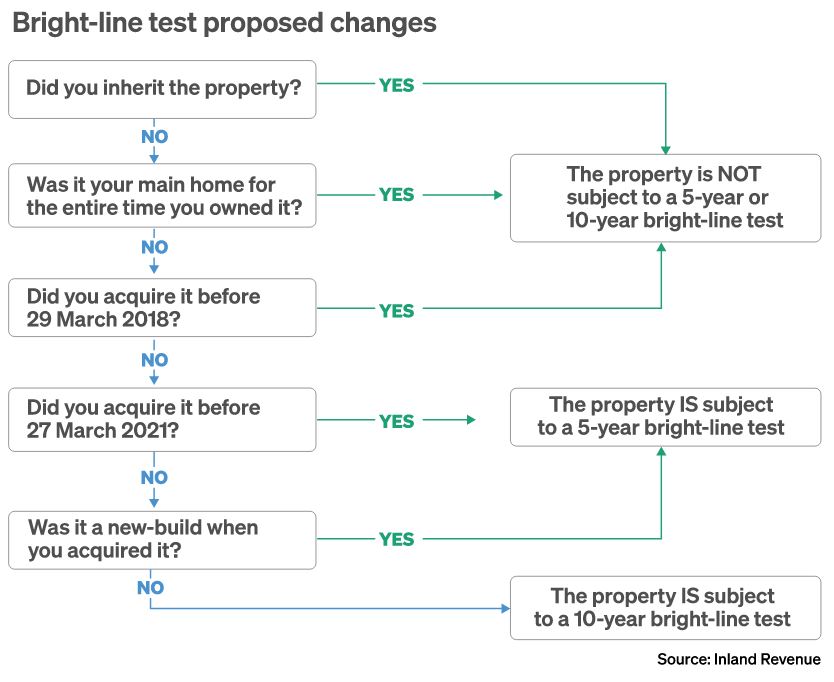

Part of the government’s plan to cool New Zealand’s housing market and help first-home buyers is to extend the bright-line test from five to ten years.

The bright-line test was introduced by the National government in 2015 meaning that anyone who sold a residential property that wasn’t their main or family home within two years of purchasing it would have to pay tax on any profit from the sale.

On 29 March 2018, the bright-line test was extended by the Labour-led government from within two years to within five years of a house being brought.

Since 27 March 2021, any existing residential house purchased in addition to the main/family home is now subject to a ten-year bright-line test for existing builds.

New builds will however still be subject to a five-year bright-line test so as to encourage property investors to invest in new residential builds.

Tax deduction loophole to be closed on property investors

Property investors will no longer be able to deduct interest on loans related to investment properties by claiming it as an expense. This tax loophole was closed for investors purchasing an investment property from late March, and come 1 October, this reform will apply to all existing investment properties regardless of when they were purchased.

The government may decide to exempt new builds, however new build investment property interest deductibility will be phased out over the next four years. Watch this space.

Investors with pre-existing home loans on their investment properties purchased prior to March 27, 2021 will still be able to claim loan interest as an expense, but this ability will be gradually retracted over the next five years.

There is also talk of closing a loophole around interest-only loans for speculators, with the Reserve Bank set to report back to ministers regarding this and any debt-to-income ratio proposals (for owner/occupiers or investors) in May 2021.

Government to pay for critical infrastructure to help increase housing supply

In addition to the changes to First Home Loan and Grant assistance available to first home buyers released in March, the government announced it would set aside $3.8 billion for the Housing Acceleration Fund to make more land build-ready.

According to Housing Minister Megan Woods, the fund will help jump-start housing developments by covering the critical infrastructure that is currently holding up development — roads and pipes to homes. Property developers aren’t altogether sold on the impact of the fund, however.

An additional $2 billion will be borrowed by the Kāinga Ora Land Programme, which will focus on government land purchases to scale up public housing supply.

Drop us a line

If the recent changes are causing you concern, feel free to get in touch with the McPherson Property Management team to discuss your options and the property management services we provide.